Understanding Florida's PIP No-Fault Medical Benefits

Discover how Florida's PIP no-fault insurance works to cover medical expenses following an auto accident. Learn the steps to file a claim, common mistakes to avoid, and when to seek legal help. Call Florida Immigration Lawyers at 1-844-967-3536 for a free consultation.

Florida's PIP no-fault insurance provides essential medical benefits for those injured in auto accidents, regardless of fault. Key takeaways:

- $10,000 minimum coverage for medical expenses

- 14-day deadline for initial treatment

- Covers 80% of medical costs

- Applies to drivers and passengers

Introduction

Imagine you're driving through Kissimmee, Florida, and suddenly you're involved in an auto accident. In Florida, Personal Injury Protection (PIP) no-fault insurance plays a crucial role in covering your medical expenses, regardless of who caused the accident. This article explains how PIP works, what medical benefits you can expect, and how to navigate the process. Call Florida Immigration Lawyers at 1-844-967-3536 for a free consultation.

Auto accidents can be disorienting and stressful, often leaving victims with immediate physical pain and a looming sense of financial uncertainty. Florida's PIP system aims to alleviate some of this burden by ensuring that medical care is accessible without the lengthy delays often associated with determining fault. This immediate access to treatment is vital for recovery and can prevent minor injuries from escalating into more severe, chronic conditions.

Understanding your rights and the steps involved in accessing these benefits is paramount. Many individuals, especially newcomers to Florida or those unfamiliar with its unique insurance laws, can find the process overwhelming. This comprehensive guide will break down the intricacies of PIP, offering practical advice and highlighting common pitfalls to avoid, ensuring you are well-prepared should you ever need to file a claim.

What is PIP No-Fault Insurance?

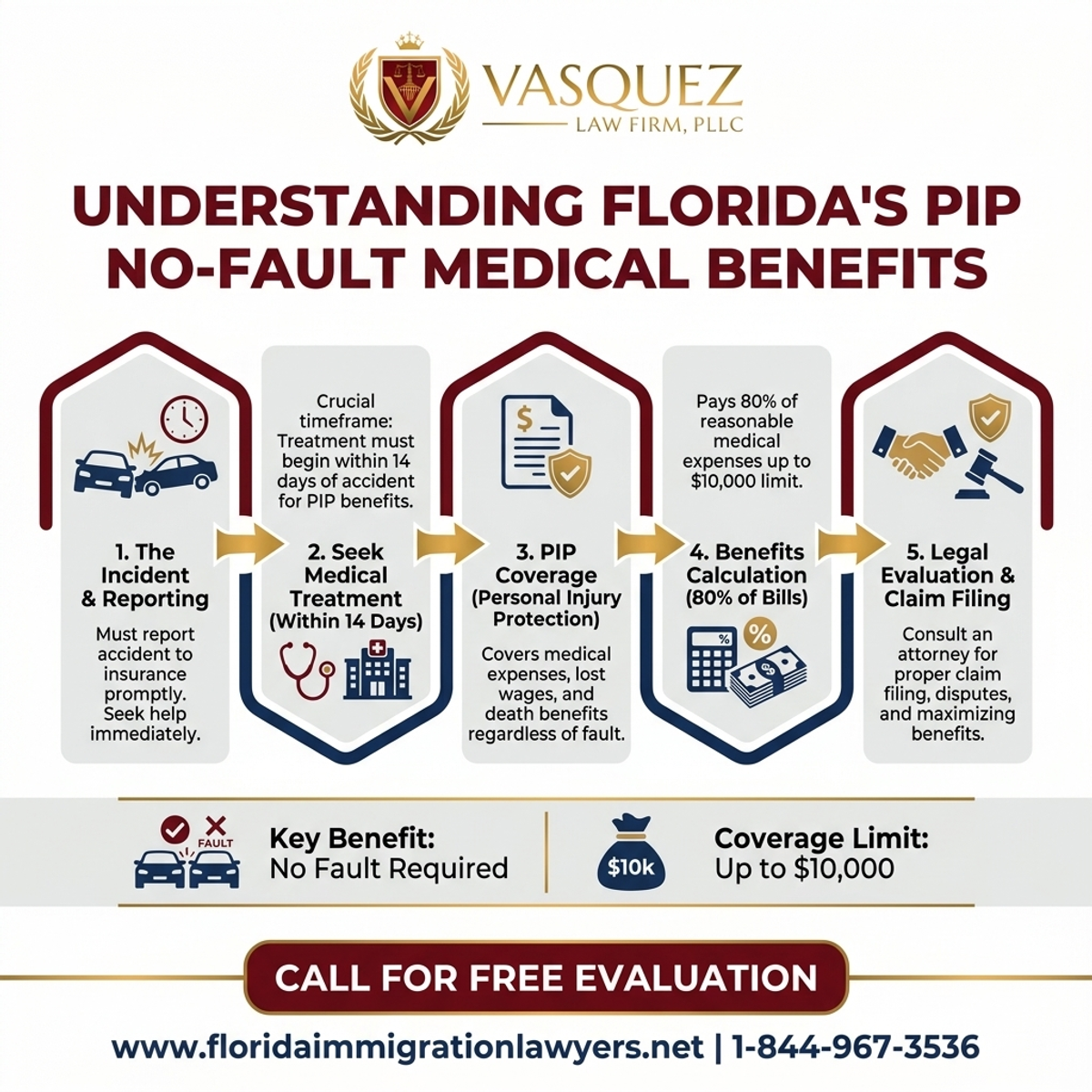

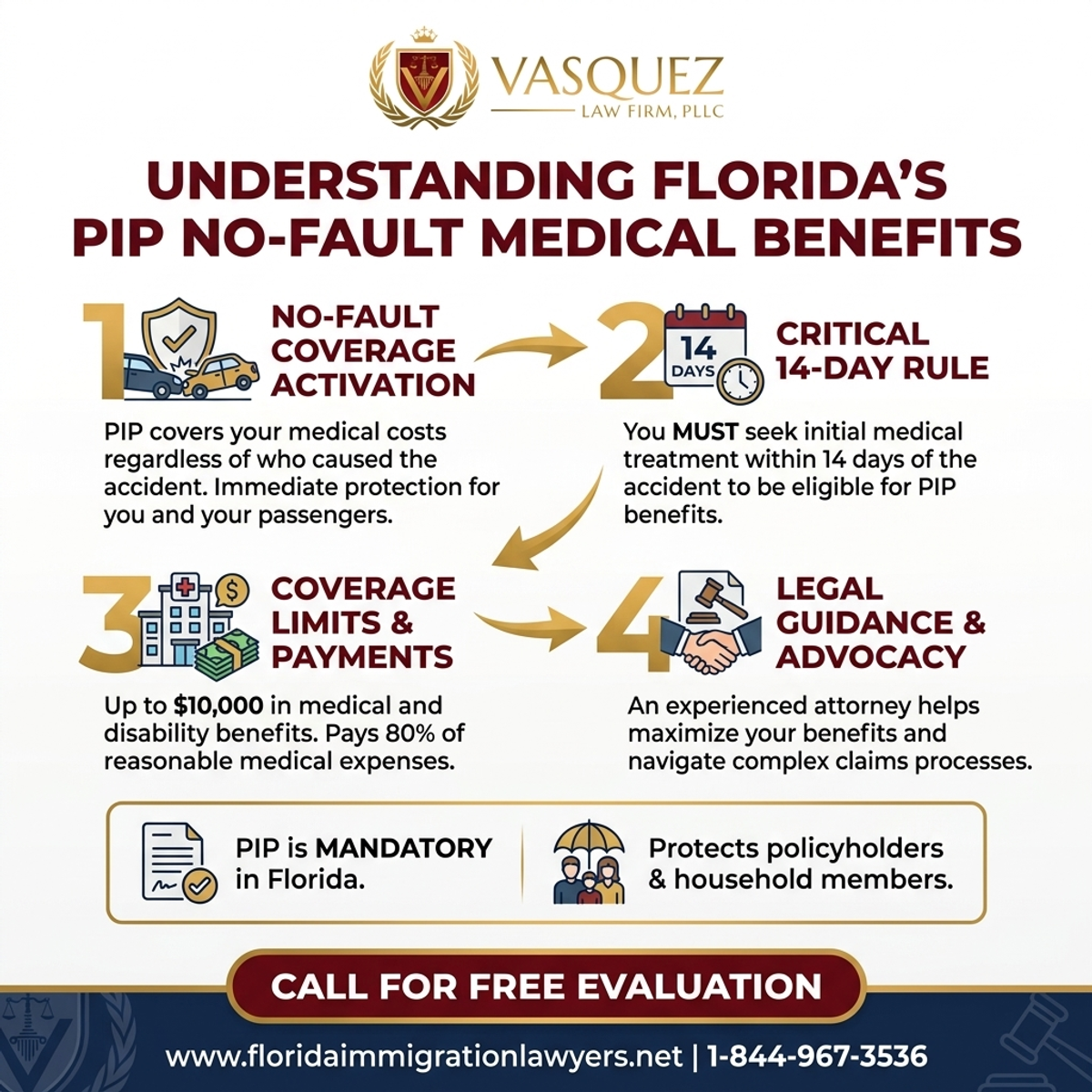

Florida's PIP no-fault insurance is designed to ensure that individuals involved in auto accidents can receive immediate medical care without waiting for a determination of fault. Under §627.736, every Florida driver must carry at least $10,000 in PIP coverage. This insurance covers 80% of necessary medical expenses, allowing for prompt treatment and recovery.

The "no-fault" aspect is a cornerstone of Florida's auto insurance system. It means that after an accident, your own insurance company pays for your medical expenses and lost wages up to your policy limits, regardless of who was at fault for the collision. This system was established to reduce litigation over minor injuries and expedite the compensation process, ensuring accident victims can focus on their recovery rather than immediate legal battles.

While PIP covers 80% of medical costs, it's important to understand the remaining 20% is typically your responsibility, often referred to as a co-payment or deductible. Additionally, PIP coverage extends beyond just emergency room visits, encompassing a range of services from follow-up doctor appointments and physical therapy to prescription medications and diagnostic tests. However, there are specific limitations and requirements, such as the 14-day rule for initial treatment, which must be strictly adhered to for your claim to be valid.

This system contrasts sharply with "at-fault" states, where the injured party must prove the other driver's negligence before receiving compensation. While Florida's no-fault system streamlines initial medical care, it's crucial to remember that it primarily covers minor to moderate injuries. For severe injuries that exceed PIP limits or result in permanent impairment, you may still be able to pursue a claim against the at-fault driver, a complex process where the guidance of experienced attorneys like Florida Immigration Lawyers can be invaluable.

Who is Covered by PIP?

PIP covers the policyholder, relatives residing in the same household, and passengers without their own PIP insurance. It also covers pedestrians and bicyclists struck by a vehicle. This broad coverage ensures that a wide range of individuals involved in an accident can access critical medical benefits quickly.

For instance, if you're driving your car and a friend is a passenger, and they don't have their own PIP policy, your PIP coverage would extend to them. Similarly, if your child, who lives with you, is a passenger in another vehicle and gets into an accident, your PIP policy would likely cover their injuries. This expansive reach underscores the protective nature of Florida's no-fault law, aiming to provide a safety net for many potential accident victims.

Benefits of PIP Insurance

PIP insurance is beneficial because it provides immediate funds for medical treatment, lost wages, and even death benefits, ensuring that financial concerns don't delay necessary care. Beyond medical expenses, PIP can also cover 60% of lost wages if your injuries prevent you from working, up to your policy limit, providing crucial financial stability during recovery.

In the tragic event of a fatality, PIP also includes a death benefit of $5,000, which can help cover funeral and burial expenses. These multifaceted benefits highlight PIP's role as a comprehensive initial safety net, designed to address the immediate aftermath of an accident from various angles, allowing individuals and their families to focus on healing and rebuilding.

Step-by-Step Guide to Accessing PIP Benefits

- Report the Accident: Contact your insurance company as soon as possible to report the accident and initiate your PIP claim.

- Seek Medical Attention: Visit a healthcare provider within 14 days to be eligible for PIP benefits.

- Submit Medical Bills: Forward all related medical bills to your insurance company for reimbursement.

- Follow Up: Keep track of your claim's progress and ensure that all paperwork is submitted promptly.

Reporting the accident promptly is not just a formality; it's a critical first step. Insurance companies require timely notification to process claims efficiently. Providing accurate details of the accident, including the date, time, location, and a brief description of what happened, will help your insurer open a claim file and guide you through the next steps. Delaying this report can raise questions about the legitimacy of your injuries and potentially jeopardize your claim.

The 14-day deadline for seeking medical attention is arguably the most crucial aspect of your PIP claim. This isn't just a recommendation; it's a strict statutory requirement in Florida. Failure to receive initial medical treatment from a qualified provider—such as an MD, DO, chiropractor, or dentist—within two weeks of the accident will result in a complete denial of your PIP medical benefits. Even if you feel fine initially, it's always wise to get checked out, as some injuries manifest days or even weeks later.

Once you've received medical care, diligently collecting and submitting all medical bills and records to your insurance company is essential. This includes invoices from emergency room visits, doctor's appointments, physical therapy sessions, and prescription receipts. Ensure that all documentation clearly links your treatment to the accident. Keeping a personal log of all appointments, treatments, and expenses can also be incredibly helpful in managing your claim and ensuring nothing is overlooked.

Step-by-Step Process — Understanding Florida's PIP No-Fault Medical Benefits

Document Checklist for PIP Claims

- Accident report

- Medical records and bills

- Insurance policy details

- Proof of lost wages, if applicable

Thorough documentation is the backbone of a successful PIP claim. The accident report, typically filed by law enforcement, serves as an an official record of the incident. It often includes crucial details like the date, time, location, parties involved, and sometimes even initial observations of injuries or vehicle damage. Obtaining a copy of this report as soon as it's available can significantly streamline your claim process.

Your medical records and bills are paramount as they directly substantiate your injuries and the costs associated with your treatment. This includes everything from the initial diagnostic reports and doctor's notes to invoices for physical therapy, specialist consultations, and prescription medications. It’s vital to ensure these documents clearly indicate the date of service, the provider, the specific treatments rendered, and that they relate directly to the accident. Maintaining organized copies for yourself, in addition to sending them to your insurer, is a smart practice.

Understanding your own insurance policy details is also critical. This includes knowing your coverage limits, any deductibles you might have, and the specific terms and conditions of your PIP policy. While your insurance company will have this information, being familiar with it yourself empowers you to track your benefits usage and anticipate potential out-of-pocket expenses. If you're claiming lost wages, detailed proof such as employer statements, pay stubs, and a doctor's note verifying your inability to work are indispensable. These documents must clearly demonstrate the income you've lost due to your accident-related injuries.

Timeline and Processing Expectations

Once you file a PIP claim, your insurance company should respond within 30 days. Delays can occur if documentation is incomplete, so ensure all necessary information is provided. Typically, medical providers are paid directly by the insurance company.

While the 30-day response time is standard for an initial acknowledgment, the entire claims process can vary. Factors like the complexity of your injuries, the number of medical providers involved, and the efficiency of your medical providers in submitting bills can all influence the timeline. It's not uncommon for claims involving extensive treatment to take several months to fully process and for all bills to be paid.

To minimize delays, proactive communication with both your insurance company and your medical providers is key. Regularly follow up to confirm that bills have been sent and received, and respond promptly to any requests for additional information from your insurer. If you encounter unreasonable delays or feel your claim is being unfairly processed, this is a clear sign to consult with a legal professional. Florida Immigration Lawyers are adept at navigating these complex situations and can advocate on your behalf to ensure timely and fair processing of your benefits.

Key Statistics — Understanding Florida's PIP No-Fault Medical Benefits

Cost Factors and Fee Breakdown

The cost of PIP insurance varies based on the insurance provider and the coverage limits you select. Remember, PIP covers up to 80% of your medical bills, so you may still be responsible for the remaining 20% and any bills exceeding your coverage limits.

Understanding your policy's deductible is also crucial. A deductible is the amount you must pay out-of-pocket before your PIP coverage begins to pay for medical expenses. For example, if you have a $1,000 deductible, you would pay the first $1,000 of your medical bills, and then PIP would cover 80% of the remaining costs up to your policy limit. Choosing a higher deductible can lower your premium, but it also means a greater initial out-of-pocket expense after an accident.

Furthermore, the $10,000 minimum PIP coverage can quickly be exhausted in cases of more serious injuries, especially considering the 20% co-payment. If your medical expenses exceed your PIP limits, you will be personally responsible for those additional costs, unless you have supplemental health insurance or can pursue a claim against an at-fault driver for severe injuries. This is why it's essential to review your auto insurance policy regularly and consider increasing your PIP limits or adding medical payments (MedPay) coverage for extra protection.

Do not navigate this process alone. Contact Florida Immigration Lawyers today.

Common Mistakes to Avoid When Using PIP

- Missing the 14-Day Deadline: Failing to seek medical treatment within 14 days can disqualify you from PIP benefits. This strict deadline is non-negotiable under Florida law, emphasizing the importance of immediate medical evaluation, even for seemingly minor aches, as injuries can worsen or become apparent days after an accident.

- Not Reporting the Accident: Delays in reporting can complicate your claim process. Notify your insurance company as soon as reasonably possible after the accident, ideally within a few days. Prompt reporting helps establish the timeline of events and prevents your insurer from questioning the validity or cause of your injuries.

- Incomplete Documentation: Missing paperwork can lead to claim denials or delays. Keep meticulous records of everything related to your accident—police reports, medical bills, doctor's notes, prescription receipts, and communication with your insurer. Organized documentation ensures a smooth review process and strengthens your claim.

- Not Understanding Coverage Limits: Assuming all costs are covered can result in unexpected out-of-pocket expenses. Familiarize yourself with your PIP policy's $10,000 limit, deductibles, and co-payments. This knowledge helps you anticipate your financial responsibilities and plan for any costs that exceed your coverage.

- Ignoring Follow-Up Care: Skipping recommended treatments can affect your health and claim. Adhering to your doctor's treatment plan, including physical therapy or specialist visits, is crucial for both your recovery and demonstrating the necessity of your medical care to your insurance company.

- Not Consulting with a Lawyer: Legal guidance can help navigate complex claims. If your claim is denied, delayed, or you have sustained serious injuries, a personal injury attorney can protect your rights, negotiate with insurers, and pursue additional compensation beyond PIP limits.

- Accepting Initial Settlements: Insurance companies may offer low settlements; consider consulting a lawyer before accepting. An early offer might not fully cover your future medical needs or lost wages. A legal expert, like those at Florida Immigration Lawyers, can evaluate the fairness of any settlement offer.

When to Call a Lawyer

If you're facing challenges with your PIP claim, such as delays or denials, it's crucial to seek legal assistance. Florida Immigration Lawyers can help you understand your rights and ensure you receive the benefits you're entitled to. Our legal team is experienced in handling such cases and can provide the guidance you need.

Beyond delays and denials, there are several other scenarios where legal counsel becomes indispensable. If your injuries are severe, permanent, or exceed the $10,000 PIP limit, you may have grounds to pursue a claim against the at-fault driver. Navigating these "serious injury" thresholds in Florida requires a deep understanding of personal injury law, which a skilled attorney can provide.

Furthermore, if you are being pressured by insurance adjusters, asked to provide recorded statements, or feel overwhelmed by the paperwork and negotiations, a lawyer can step in to protect your interests. An attorney from Florida Immigration Lawyers can handle all communications, gather necessary evidence, and build a strong case to ensure you receive maximum compensation for your medical expenses, lost wages, pain, and suffering. Don't hesitate to call 1-844-967-3536 for a free consultation if you find yourself in any of these challenging situations.

Frequently Asked Questions About Florida PIP

This section addresses common questions about Florida's Personal Injury Protection (PIP) insurance, providing clear and concise answers to help you better understand your coverage and rights after an auto accident.

What is the difference between PIP and Bodily Injury (BI) liability coverage?

PIP (Personal Injury Protection) covers your own medical expenses and lost wages regardless of fault, up to your policy limits. Bodily Injury (BI) liability coverage, on the other hand, pays for the medical expenses and lost wages of *others* if you are at fault for an accident. Florida requires PIP but not BI, though BI is highly recommended for comprehensive protection.

Can I choose my own doctor under PIP?

Generally, yes, you have the right to choose your own medical provider for PIP-covered treatments, as long as they are licensed and qualified to treat your injuries. However, your insurance company may require you to attend an independent medical examination (IME) with a doctor of their choosing to verify the necessity and extent of your treatment.

What if my medical bills exceed my $10,000 PIP limit?

If your medical bills surpass your $10,000 PIP limit, you become personally responsible for the excess costs. In such cases, your private health insurance may cover the remaining balance. If your injuries are deemed "permanent" or "serious" under Florida law, you may also be able to file a personal injury lawsuit against the at-fault driver to recover damages beyond PIP, including pain and suffering.

Does PIP cover chiropractic care or acupuncture?

Yes, Florida's PIP statute allows for coverage of medically necessary chiropractic services, as well as acupuncture, massage therapy, and other rehabilitative services, provided they are prescribed by a qualified healthcare professional. However, these treatments must be directly related to the accident injuries and must be initiated within the 14-day window to be eligible for coverage.

About Florida Immigration Lawyers

Sources and References

- U.S. Citizenship and Immigration Services (USCIS)

- Executive Office for Immigration Review (EOIR)

- U.S. Department of State - Bureau of Consular Affairs

- Immigration and Nationality Act (INA), 8 U.S.C. Chapter 12

Do Not Navigate This Process Alone

Our experienced immigration attorneys are ready to fight for you. Get a free, confidential consultation today.

Se Habla Español

Frequently Asked Questions

Florida Immigration Lawyers

Immigration Attorney | Founder, Vasquez Law Firm

U.S. Air Force veteran and immigration attorney with thousands of cases resolved. J.D., NCCU School of Law. AILA member. Admitted to the 4th, 5th, and 11th Circuit Courts.

Available 24/7 - Free Evaluations

Related Legal Services

Our Florida immigration attorneys can help you with Florida wrongful death claims, Florida personal injury attorney Harold Estrada-Rodriguez and free personal injury consultation. Call today at 1-844-967-3536 for a free consultation.

Related Links

Related Topics

Free Legal Consultation

Discuss your case with our experienced attorneys. We're available 24/7.

Se Habla Español - Estamos aquí para ayudarle.

Related Articles

Florida Wrongful Death Survivor Damages Explained | VLF Florida

Learn about Florida's wrongful death statutes, specifically §§768.16-768.21, which outline compensation for survivors. Call for a free consultation.

Understanding Florida's 2-Year Statute of Limitations

Navigating Florida's 2-year statute of limitations for personal injury claims is crucial. Learn about recent changes under HB 837 and how they affect your rights. Call Florida Immigration Lawyers for a free consultation.

Truck Driver Fatigue & HOS Violations: Florida Accidents

Truck driver fatigue and Hours of Service (HOS) violations are critical factors in severe Florida truck accidents. When commercial drivers fail to adhere to FMCSA regulations, their impaired judgment and reaction times can lead to catastrophic collisions. This comprehensive guide explores federal HOS rules, how fatigue contributes to accidents, and the vital steps victims should take after a crash in Fort Lauderdale, Orlando, or Kissimmee. Learn about proving negligence, seeking compensation for injuries, and avoiding common mistakes. Florida Immigration Lawyers, with Harold Estrada-Rodriguez (Florida Bar No. 1041171) handling personal injury matters, offers dedicated legal representation on a 'no recovery, no fee' basis. Contact us today for a free consultation and let us fight for your rights.

Low Insurance Settlement Early Offer Florida Advice

If you've suffered a personal injury in Florida and received a low insurance settlement early offer, it's critical to understand your rights before accepting anything. Insurance companies often make quick, low offers to minimize their payouts, hoping you'll settle before realizing your claim's true value. This comprehensive guide explains why these offers are made, the common tactics insurers use, and the crucial steps you should take, including seeking prompt medical attention and gathering all necessary documentation. Learn about Florida's specific personal injury laws, such as the two-year statute of limitations and comparative negligence rules. Discover how a skilled Florida personal injury attorney can help you accurately calculate your damages, negotiate effectively, and fight for the maximum compensation for medical bills, lost wages, and pain and suffering. Don't let a lowball offer prevent you from getting the justice you deserve. Contact Florida Immigration Lawyers for a free consultation to discuss your case and protect your future.