Understanding Florida PIP No-Fault Medical Benefits

Learn how Florida's PIP no-fault insurance provides essential medical benefits after an accident. Understand coverage, common mistakes, and when to seek legal help. Contact Florida Immigration Lawyers at 1-844-967-3536 today!

Understanding Florida PIP No-Fault Medical Benefits

Florida's Personal Injury Protection (PIP) insurance, often referred to as "no-fault" insurance, is a critical component of the state's motor vehicle insurance laws. Designed to ensure that individuals injured in car accidents receive prompt medical care regardless of who was at fault, PIP provides essential benefits for medical expenses, lost wages, and even death benefits. Navigating the intricacies of Florida PIP can be challenging, especially when dealing with the aftermath of an accident. This comprehensive guide aims to demystify the Florida PIP no-fault medical benefits system, helping you understand your rights and responsibilities.

What is Florida PIP No-Fault?

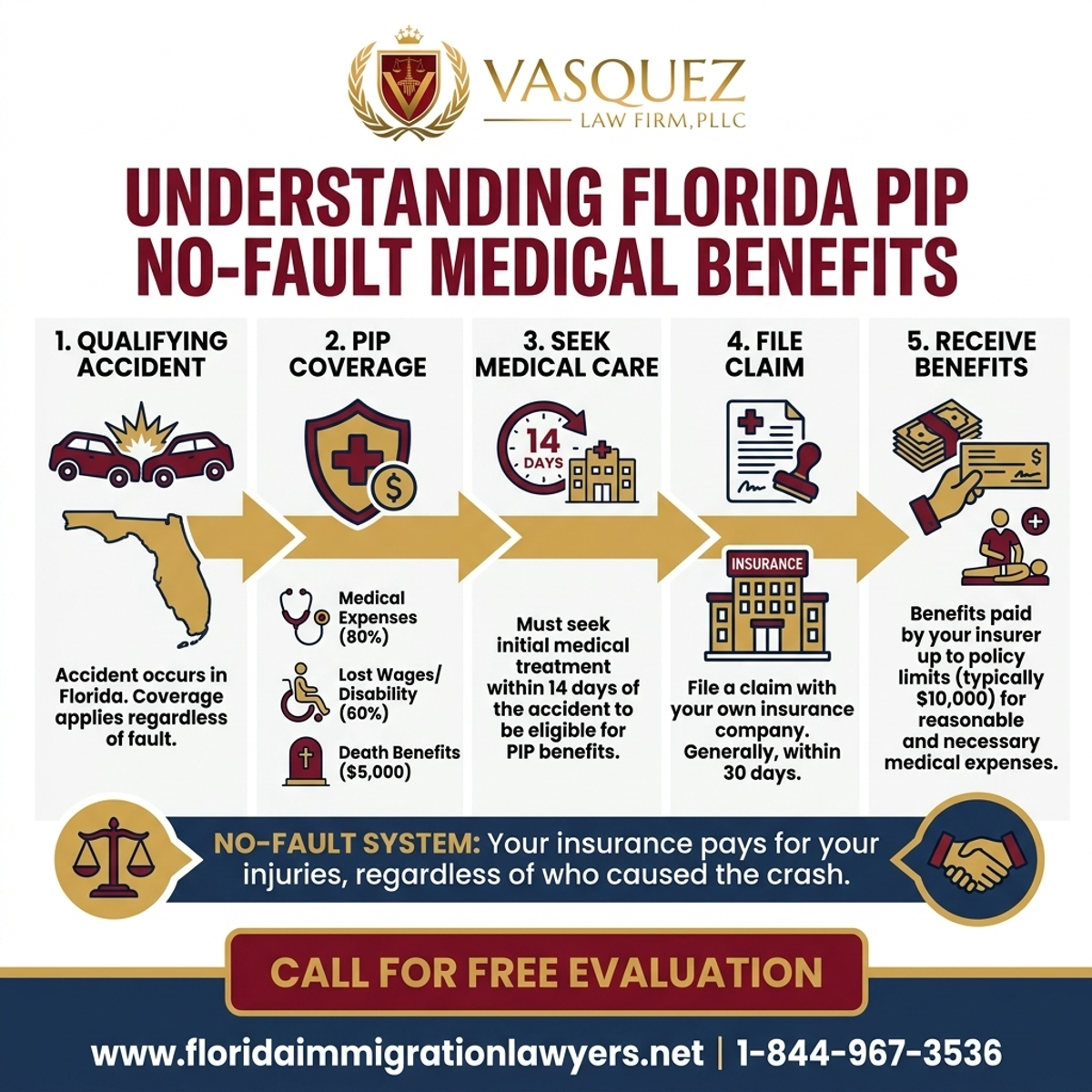

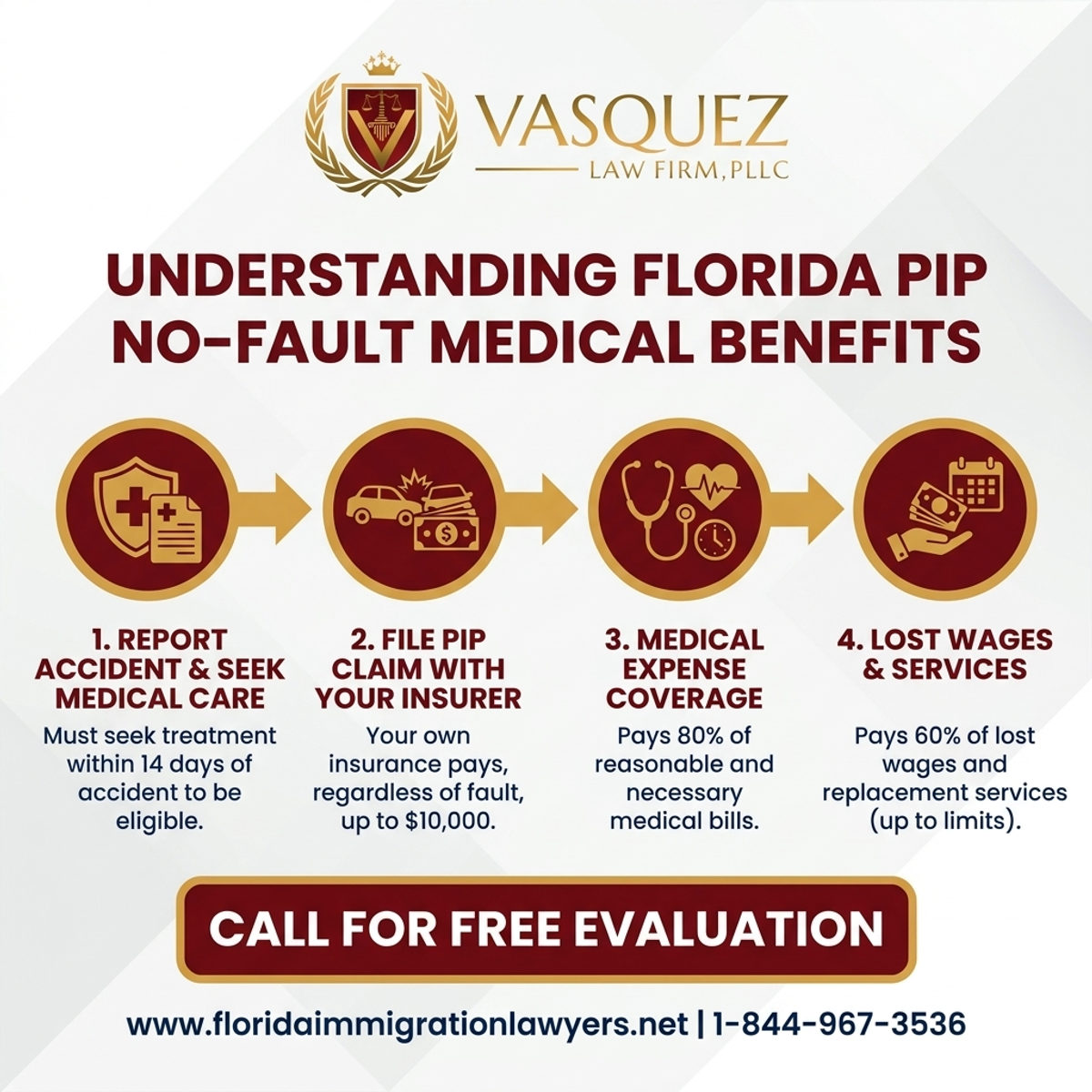

Florida operates under a no-fault insurance system, meaning that after a car accident, your own insurance company (specifically your PIP coverage) is responsible for paying a portion of your medical expenses and lost wages, regardless of who caused the accident. This system is designed to streamline the process of getting immediate medical care and reduce the number of minor personal injury lawsuits. Every driver in Florida is required to carry a minimum of $10,000 in PIP coverage. This coverage extends to the policyholder, household members, and certain passengers, as well as pedestrians and cyclists hit by your vehicle. The primary goal of PIP is to provide quick access to funds for medical treatment, ensuring that accident victims can focus on recovery without immediate financial stress. It covers 80% of your reasonable and necessary medical expenses and 60% of your lost wages, up to your policy limit, after any applicable deductible. Understanding the scope and limitations of this coverage is the first step toward effectively utilizing your benefits following an accident in the Sunshine State.

Key Aspects of PIP Medical Benefits

Understanding the specific parameters of your PIP medical benefits is crucial for maximizing your coverage after an accident. Florida Statute § 627.736 outlines the requirements and limitations of PIP coverage, providing up to $10,000 in benefits for medical expenses and lost wages. However, accessing these benefits isn't always straightforward, and several key factors dictate the extent of your coverage.

Emergency Medical Condition (EMC) vs. Non-EMC

A significant distinction in Florida PIP law is whether your injuries are classified as an Emergency Medical Condition (EMC). If a physician, osteopathic physician, or dentist determines you have an EMC, you are eligible for the full $10,000 in medical benefits. If no EMC is determined, your medical benefits are capped at $2,500. This determination is critical, as it directly impacts the financial support available for your recovery. It underscores the importance of seeking immediate medical attention and ensuring a thorough diagnosis.

The 14-Day Rule

To be eligible for any PIP medical benefits, you must seek initial medical treatment within 14 days of the motor vehicle accident. This rule applies to all types of medical providers, including hospitals, emergency rooms, urgent care clinics, and primary care physicians. Failure to seek treatment within this strict timeframe will result in a complete loss of your PIP medical benefits, regardless of the severity of your injuries. This emphasizes the urgency of medical evaluation post-accident.

Deductibles and Co-pays

While PIP is often called "no-fault," it doesn't mean you pay nothing. Most PIP policies include a deductible, which is the amount you must pay out-of-pocket before your PIP coverage begins. Common deductibles range from $250 to $1,000. After the deductible is met, PIP typically covers 80% of your reasonable and necessary medical expenses and 60% of lost wages, up to the policy limit. The remaining percentage is your co-pay.

Types of Covered Medical Services

PIP covers a wide range of medically necessary services, including:

- Ambulance transportation

- Hospitalization and emergency room visits

- Physician services (including specialists)

- Chiropractic services

- Physical therapy and rehabilitation

- Diagnostic services (X-rays, MRIs, CT scans)

- Prescription medications

- Dental treatment (if related to the accident)

However, certain services, such as acupuncture or massage therapy, may require specific documentation or referral to be covered.

Exclusions and Limitations

It's important to be aware of what PIP does not cover. For instance, injuries sustained while riding a motorcycle are generally not covered under standard auto PIP policies, as motorcycles have their own insurance requirements. Similarly, accidents occurring out-of-state may be subject to the laws of that state, though Florida PIP can sometimes extend limited coverage. Understanding these nuances is vital for managing expectations and planning your recovery.

Navigating the PIP Claim Process

Initiating and managing a PIP claim can be a complex endeavor, requiring careful attention to detail and timely action. The steps you take immediately following an accident, and in the days and weeks thereafter, significantly impact the success of your claim.

Immediate Steps After an Accident

Your first priority should always be your health and safety. Seek medical attention promptly, even if you feel your injuries are minor. As mentioned, the 14-day rule is non-negotiable for PIP eligibility. Report the accident to your insurance company as soon as possible, typically within a few days. Provide them with accurate details but avoid making speculative statements about fault or the extent of your injuries. Remember, anything you say can be used by the insurer.

Documentation is Key

Maintain meticulous records of everything related to your accident and recovery. This includes:

- Police reports

- Contact information for all parties involved and witnesses

- Photos of the accident scene and vehicle damage

- All medical records, bills, and receipts from doctors, hospitals, and pharmacies

- Records of lost wages from your employer

- Correspondence with your insurance company

Step-by-Step Process — Understanding Florida PIP No-Fault Medical Benefits

Thorough documentation provides concrete evidence to support your claim and helps prevent disputes over the necessity or cost of treatment.

Dealing with Insurance Adjusters

Insurance adjusters are trained to minimize payouts. While they may seem helpful, their primary goal is to protect the insurance company's bottom line. Be cautious about providing recorded statements without legal counsel, and never sign anything without fully understanding its implications. Focus on providing factual information and direct them to your medical providers for details about your injuries and treatment plan. If you feel overwhelmed or that your claim is being unfairly scrutinized, it's a strong indicator that you should consult with legal professionals.

When PIP Benefits Are Denied or Reduced

Despite Florida's no-fault system, it's not uncommon for PIP benefits to be denied, delayed, or significantly reduced by insurance companies. These actions can leave accident victims in a precarious financial situation, struggling to pay for necessary medical care.

Common Reasons for Denial or Reduction

- Failure to meet the 14-day rule: The most straightforward reason for denial.

- Lack of EMC determination: If your injuries aren't deemed an Emergency Medical Condition, benefits may be capped at $2,500, leading to a "reduction" from the full $10,000.

- Treatment deemed "not reasonable and necessary": Insurance companies often challenge the necessity or cost of medical treatments, arguing they are excessive or unrelated to the accident.

- Policy exclusions: As discussed, certain situations or types of vehicles may not be covered.

- Late filing or incomplete documentation: Missing deadlines or providing insufficient paperwork can lead to claim rejections.

- Pre-existing conditions: Insurers may try to attribute your injuries to a pre-existing condition rather than the accident.

What to Do If Benefits Are Denied

If your PIP benefits are denied or reduced, do not despair. You have options.

- Review the denial letter: Understand the specific reason provided by the insurer.

- Gather supporting documentation: Work with your medical providers to obtain detailed reports justifying the necessity of your treatment and the diagnosis of an EMC, if applicable.

- Appeal the decision: You can formally appeal the insurer's decision, often with the help of an attorney.

- Consider legal action: If an appeal is unsuccessful or the insurer refuses to negotiate fairly, a lawsuit may be necessary to compel them to pay the benefits you are owed. An experienced attorney can help challenge the insurer's assessment of "reasonable and necessary" care and fight for your rights.

Beyond PIP: Seeking Additional Compensation

While Florida's PIP system is designed to provide immediate medical benefits, its $10,000 limit often falls short of covering all expenses, especially in cases of serious injury. When your medical bills, lost wages, and pain and suffering exceed PIP coverage, you may be able to seek additional compensation from the at-fault driver.

The "Serious Injury" Threshold

Florida is a tort state with a no-fault overlay. This means that to step outside the no-fault system and sue the at-fault driver for non-economic damages (like pain and suffering) and additional economic damages, you must meet a specific "serious injury" threshold. Florida Statute § 627.737 defines a permanent injury as:

- Significant and permanent loss of an important bodily function.

- Permanent injury within a reasonable degree of medical probability, other than scarring or disfigurement.

- Significant and permanent scarring or disfigurement.

- Death.

Meeting this threshold is often a point of contention with insurance companies and typically requires strong medical evidence.

Key Statistics — Understanding Florida PIP No-Fault Medical Benefits

Bodily Injury (BI) Liability Claims

If the at-fault driver carries Bodily Injury (BI) liability insurance, you can file a claim against their policy once you meet the serious injury threshold. BI coverage pays for the medical expenses, lost wages, pain and suffering, and other damages of the injured party in an accident caused by the policyholder. The amount you can recover depends on the at-fault driver's policy limits.

Uninsured/Underinsured Motorist (UM/UIM) Coverage

What if the at-fault driver has no BI insurance or insufficient coverage to compensate you fully? This is where your own Uninsured/Underinsured Motorist (UM/UIM) coverage becomes invaluable. UM/UIM protects you and your passengers if you're hit by a driver with no insurance (uninsured) or not enough insurance (underinsured) to cover your damages. This coverage acts as a safety net, allowing you to recover damages that would otherwise be uncollectible. It's a highly recommended addition to any auto insurance policy.

Wrongful Death Claims

In the tragic event that an accident results in a fatality, Florida law allows the personal representative of the deceased's estate to file a wrongful death claim. This type of claim seeks compensation for medical and funeral expenses, lost income, loss of companionship, and pain and suffering of the survivors. These cases are complex and require compassionate, expert legal guidance.

The Role of a Florida Car Accident Attorney

Navigating the aftermath of a car accident in Florida, from understanding PIP benefits to pursuing claims against at-fault drivers, can be overwhelming. This is where the expertise of a dedicated car accident attorney becomes invaluable.

Why Legal Representation is Crucial

An attorney acts as your advocate, protecting your rights and interests against powerful insurance companies. They understand the nuances of Florida's no-fault laws, the serious injury threshold, and how to effectively negotiate for maximum compensation.

Assisting with PIP Claims

Even with PIP, an attorney can help ensure your claim is filed correctly, all necessary documentation is submitted, and that your medical treatments are properly classified to maximize your benefits. They can challenge unfair denials or reductions, ensuring you receive the medical care you need.

Negotiating with Insurance Companies

Insurance adjusters are skilled negotiators. Without legal representation, you may unknowingly accept a settlement that is far less than your case is worth. An attorney will handle all communications, gather evidence, build a strong case, and negotiate fiercely on your behalf to secure a fair settlement that covers all your damages, including medical bills, lost wages, pain and suffering, and future care.

Litigation if Necessary

While most personal injury cases settle out of court, if a fair settlement cannot be reached, your attorney will be prepared to take your case to trial. They will represent you in court, present your evidence, cross-examine witnesses, and argue your case to a jury, fighting to achieve the justice you deserve.

Protecting Your Rights

Beyond the immediate financial aspects, a lawyer ensures your legal rights are protected at every stage of the process, from the initial accident report to the final resolution of your claim. This includes advising on potential pitfalls, ensuring compliance with all legal deadlines, and preventing you from inadvertently harming your case. Our firm offers comprehensive legal services, extending beyond personal injury to areas such as immigration law, including asylum cases and deportation defense. Our diverse team of experienced attorneys is committed to providing exceptional legal support across various complex legal challenges. Don't face the complexities of the legal system alone. Contact

Sources and References

- U.S. Citizenship and Immigration Services (USCIS)

- Executive Office for Immigration Review (EOIR)

- U.S. Department of State - Bureau of Consular Affairs

- Immigration and Nationality Act (INA), 8 U.S.C. Chapter 12

Do Not Navigate This Process Alone

Our experienced immigration attorneys are ready to fight for you. Get a free, confidential consultation today.

Se Habla Español

Frequently Asked Questions

Florida Immigration Lawyers

Immigration Attorney | Founder, Vasquez Law Firm

U.S. Air Force veteran and immigration attorney with thousands of cases resolved. J.D., NCCU School of Law. AILA member. Admitted to the 4th, 5th, and 11th Circuit Courts.

Available 24/7 - Free Evaluations

Related Legal Services

Our Florida immigration attorneys can help you with Florida wrongful death claims, Florida personal injury attorney Harold Estrada-Rodriguez and free personal injury consultation. Call today at 1-844-967-3536 for a free consultation.

Related Links

Related Topics

Free Legal Consultation

Discuss your case with our experienced attorneys. We're available 24/7.

Se Habla Español - Estamos aquí para ayudarle.

Related Articles

Florida Wrongful Death Survivor Damages Explained | VLF Florida

Explore Florida's wrongful death statutes 768.16 and 768.21 to understand survivor damages. Learn who can claim, types of compensation, and common mistakes to avoid. Contact us for expert legal guidance.

Florida Insurance Settlement: Early Offer Too Low?

Early insurance settlement offers in Florida can often be too low, leaving you with less compensation than you deserve. Learn how to negotiate effectively and ensure fair compensation for your personal injury claim. Call Florida Immigration Lawyers at 1-844-967-3536 for a free consultation.

Understanding Florida Wrongful Death Survivor Damages

Explore the intricacies of Florida's wrongful death statutes, §768.16 and §768.21, focusing on survivor damages. Learn who is eligible and what compensation can be claimed. Contact Florida Immigration Lawyers at 1-844-967-3536 for a free consultation.

Florida Pedestrian Accident Crosswalk Rights and Damages

Pedestrian accidents in Florida, especially in crosswalks, can lead to serious injuries. Learn about your rights and potential damages. Call for a free consultation today.